The latest super changes: Division 296, what it means for you, and how to adapt

The latest superannuation changes may feel like they aren’t relevant to many right now, but given the long-term nature of superannuation, the best time to plan for it is as far ahead as possible.

The recent Better Targeted Superannuation Concessions will insert a new Division 296 into the Income Tax Assessment Act 1997, with the intention of making the superannuation environment less generous in terms of tax concessions for individuals with total superannuation balances exceeding $3 million and far less generous for balances exceeding $10 million.

In this article, we’ll be covering the impact on you and the options you have.

The only constant is change (even in superannuation)

Whilst superannuation is a long-term investment for us as individuals, it’s also a long-term investment for the nation. As such, as times change, so too do the rules for superannuation.

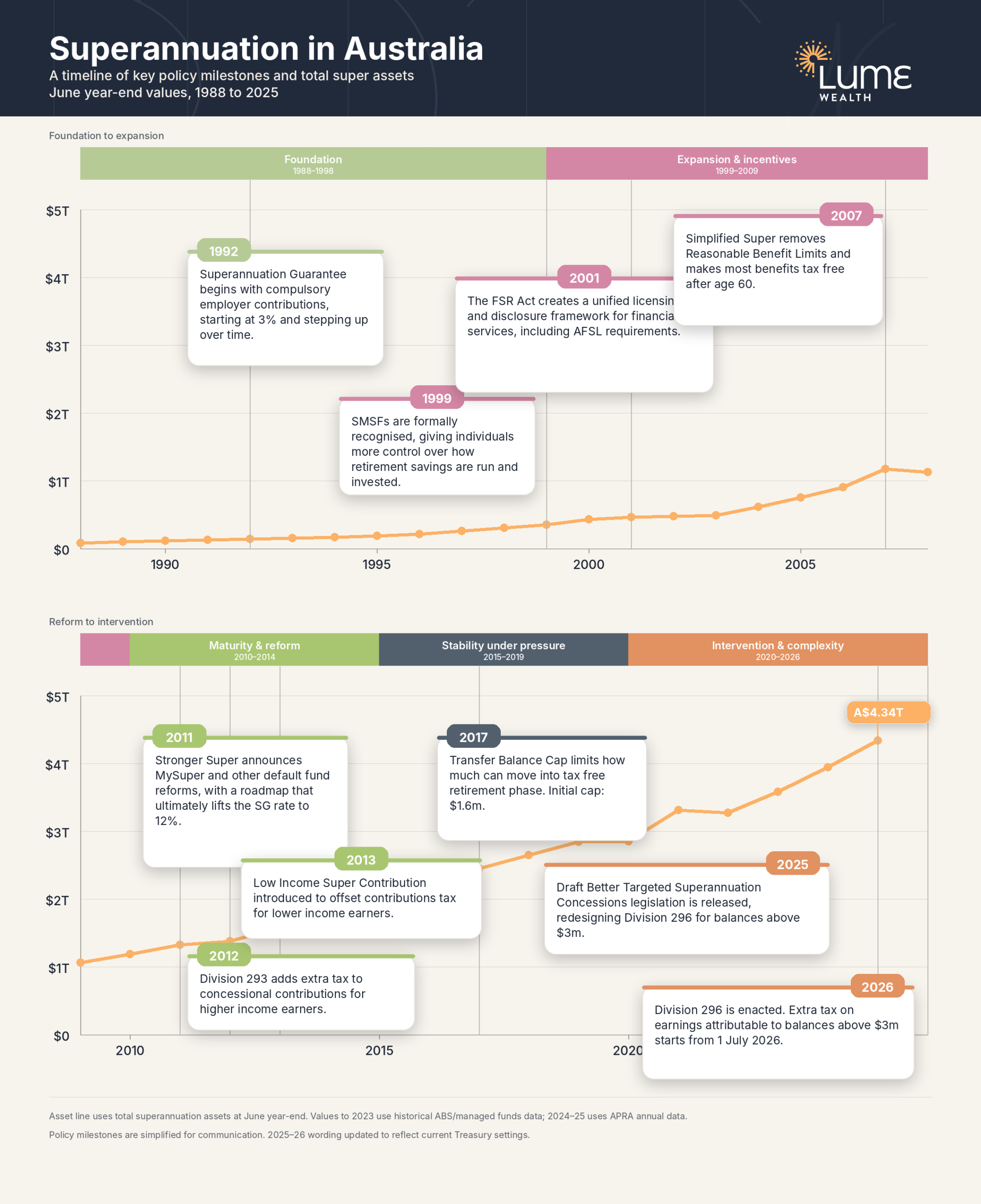

Since the introduction of the superannuation guarantee in 1992, superannuation has seen over 85 changes in policy. This is what we consider ‘Legislative risk’ and is a valid consideration when planning for the long term.

Further reading: Superannuation in Australia: a timeline via APRA

How superannuation tax concessions for earnings work

The newest changes don’t impact salary sacrifice arrangements, personal concessional contributions, tax-free pensions, or anything else to do with the generosity of funds flowing in or out of the superannuation environment.

They do however impact the taxation of earnings within superannuation.

Whilst the tax treatment of superannuation earnings are made quite opaque by many superannuation funds, investment income received in superannuation is indeed taxed. This is similar to how rental income, interest, dividends, and capital gains are taxed in your own name.

Below is a simplified version of how such tax works between your own name, superannuation in accumulation phase, and superannuation in pension phase.

| Environment | Income tax (Interest, dividends, rent) | Capital gains (Sale of investments) |

|---|---|---|

| Personal individual | Your marginal tax rate (up to 47%) | 50% discount*, then taxed at your marginal rate (up to 47%) |

| Superannuation (Accumulation phase) | 15% (unless balance is >$3M from 1 July 2026) | 1/3 discount*, then taxed at 15% (unless balance is >$3M from 1 July 2026) |

| Superannuation (Pension phase) | Tax-free | Tax-free |

* For assets held longer than 12 months

Previous changes to superannuation that took effect in 2017 placed a limit on how much funds an individual can transfer into pension phase, which at 1 July 2026 will be $2.1 million. This number is known as the Transfer Balance Cap.

This means presently, once you can reach pension phase, earnings within the pension are as generous as they can be (tax free), and earnings above that amount are still typically much better than if you held the assets personally (at only 15% tax).

In short, even without the concessional Centrelink treatment, superannuation is a very efficient vehicle to keep and invest your money.

What’s changing

From 1 July 2026, Division 296 reduces the tax concessions on very large super balances. At a high level, it applies to people with total super balances above $3 million, with a higher layer again above $10 million. The thresholds are indexed over time, and the tax is calculated by reference to earnings attributable to the excess balance.

For the politicos out there, you can read more about the changes to these bills here.

For planning purposes, the easiest way to think about super now is in layers.

Assumes a $2.1 million transfer balance cap from 1 July 2026. Illustration simplified for clarity.

First is the pension layer, where earnings on retirement-phase assets are tax free inside super, subject to the transfer balance cap.

Next is the standard accumulation layer, where earnings are generally taxed at 15% but couldn’t possibly be included in a pension where the most concessions apply.

Above $3 million, where the new Division 296 starts to apply, there is now a less concessional layer that is roughly 30% in simplified terms.

Above $10 million, there is a harsher layer again, roughly 40%.

These are not legal sub-accounts, and there is more to it in the detail, but this provides a simplified overview of how these interrelated thresholds can stack in practice.

One detail matters more than many people realise: Division 296 is worked out on total super balance, and total super balance includes both accumulation-phase account totals and retirement-phase account totals. So, moving money to pension phase can still be the right move, but it does not make that money invisible for Division 296.

Couples

Whilst finances can be a huge source of stress on relationships, when it comes to superannuation couples do have some extremely beneficial strategies and options at their disposal.

Division 296 is an individual rule, not a household rule. The transfer balance cap works the same way.

For a couple, the practical opportunity is ensuring that money spread well enough (where possible) that both people can use their own thresholds and their own pension cap. That is why early planning matters so much.

Before the threshold is relevant, there are still annual contribution caps to use, there is still time to even out balances, and there are still choices around which spouse contributes more and which spouse may eventually draw down first.

In this financial year, the concessional contribution cap is $30,000, the non-concessional contribution cap is $120,000, and spouse contribution splitting can generally move up to 85% of a financial year’s taxed splittable contributions to the other spouse. By targeting contributions of different types to the spouse with a lower balance, you can optimise your total affairs for the benefit of Division 296 tax.

Important note: There are many moving parts, including different contribution opportunities, withdrawal restrictions, Centrelink implications, and much more. It is essential to seek professional financial advice before implementing these strategies.

Penny and Samuel: Same wealth, different result

Take Penny and Samuel Wise. They are the same age. They earn the same income. They are on track to retire with $8 million in today’s dollars.

A lop-sided layer cake

Samuel had a long history of contributing the maximum available to superannuation prior to marrying Penny later in life. Penny had made healthy contributions herself, but not so much as Samuel. As a result:

- Penny’s Total Superannuation Balance: $2,000,000

- Samuel’s Total Superannuation Balance: $6,000,000

The examples below show the value of pension phase and the impact of Division 296.

| Layer | Rate | Penny | Samuel | Total | Earnings (6%) | Tax |

|---|---|---|---|---|---|---|

| Pension layer | 0% | $2,000,000 | $2,100,000 | $4,100,000 | $246,000 | $0 |

| Accumulation layer | 15% | $0 | $900,000 | $900,000 | $54,000 | $8,100 |

| Div 296 layer | 30% | $0 | $3,000,000 | $3,000,000 | $180,000 | $54,000 |

| Total | $2,000,000 | $6,000,000 | $8,000,000 | $480,000 | $62,100 |

Assumes earnings of 6% within superannuation and uses a simplified $2.1 million transfer balance cap from 1 July 2026.

When everything is balanced

Now change the split to something which may have been achievable with some long-term planning, without any change to overall household wealth: A perfectly even split of $4 million each.

| Layer | Rate | Penny | Samuel | Total | Earnings (6%) | Tax |

|---|---|---|---|---|---|---|

| Pension layer | 0% | $2,100,000 | $2,100,000 | $4,200,000 | $252,000 | $0 |

| Accumulation layer | 15% | $900,000 | $900,000 | $1,800,000 | $108,000 | $16,200 |

| Div 296 layer | 30% | $1,000,000 | $1,000,000 | $2,000,000 | $120,000 | $36,000 |

| Total | $4,000,000 | $4,000,000 | $8,000,000 | $480,000 | $52,200 |

Same total super balance, but $9,900 less tax per year. That is a 16% reduction in tax on earnings.

That is the point. For a couple, balance management changes how much of the household’s wealth sits in the 0% pension layer, how much stays in the 15% layer, and how much is exposed to Division 296.

What couples should be thinking about now

All else being equal, smart planning often means:

- Directing more contributions to the spouse with the lower balance.

- Considering contribution splitting from the spouse with the higher balance.

- Thinking carefully about which spouse should fund retirement cash flow first.

- Exploring recontribution strategies in more complex cases, with advice.

The goal in this regard, is to avoid one spouse paying extra tax while the other spouse has an under-used threshold or an under-used pension cap.

This is also where advice matters, because contribution rules, age rules, estate planning, and cash flow can all pull in different directions.

Going over later is still often a good outcome

There is no prize for staying under $3 million at all costs.

If extra contributions or strong investment returns eventually push you above the threshold, that does not mean those contributions were a mistake. The pension layer is still valuable. The standard accumulation layer is still valuable. And even the higher Division 296 layer can still compare well with outside-super options, depending on how much taxable income you already have outside super and what kind of return you expect from the portfolio.

In other words, going over later is often still a good result. It usually means the plan worked.

It is also often a reversible decision later in life. Once you meet a condition of release (commonly by retiring after reaching age 60, or by turning 65) you may be able to move money out of super if the outside-super comparison becomes more attractive.

The Div 296 change doesn’t impact tax on the withdrawal itself, only earnings within the fund.

What $4 million at retirement looks like when you can’t shuffle further

Now take a different example.

An individual has $4 million in super, has turned 60, and has retired.

The first move is usually straightforward. Start the maximum pension you can.

After that, think in layers, not account labels.

The next roughly $0.9 million still keeps total super at or below $3 million. That is usually a very attractive 15% accumulation layer.

The final roughly $1 million is the layer that deserves the closest comparison with non-super alternatives. That is where Division 296 starts to bite.

Once the best layers are full, compare the next dollar

If someone in that position has very little non-super wealth apart from the family home, direct personal ownership may be the cleanest place to invest the marginal dollar outside super.

That is especially true when outside taxable income is low. On current resident tax rates, the 30% marginal bracket starts above $45,000 of taxable income.

Individuals and trusts also generally get a 50% CGT discount on assets held for at least 12 months (at least for now). That can make direct ownership surprisingly competitive when returns are tilted more toward capital growth than current income.

But once someone already has other income-producing assets (rent, dividends, business income, or an existing portfolio) other structures can become more relevant.

- A discretionary trust can add flexibility, but beneficiaries are generally taxed on their share of the trust’s net income regardless of when or whether the cash is actually paid.

- A bucket company can cap current tax at 25% if it is a base rate entity, or 30% otherwise, but companies are not eligible for the CGT discount.

- Investment bonds are a more niche option, but earnings are taxed internally at 30% and, if no withdrawals are made in the first 10 years, no further tax is payable.

This is why the answer is rarely simple.

Some non-super money can be part of the optimal mix. Too much non-super money can make the overall result worse. The question is usually not whether super has stopped working. It is where the next dollar belongs.

Above $10 million, it becomes a different conversation

Above $10 million, the top layer becomes much less attractive again.

For planning purposes, that is the zone to think about as roughly a 40% layer. At that point, super is rarely the automatic home for new wealth. The better question is usually what should stay inside super, and what structure should hold the next dollar outside it.

Division 296 does not kill super. It just makes the top layers less generous than the ones below.

That is why the smartest move often happens well before $3 million. Use both spouses’ thresholds well. Use both spouses’ pension caps well. Fill the best layers first. Then compare the marginal dollar above that line on its own merits.

This is a complex area, and worthwhile seeking advice early if you think you may be impacted by Div 296 taxation now, soon, or even in the distant future.

Contact us to get personal advice on what may be best for your individual circumstances.

This general advice has been prepared without taking into account your objectives, financial situation or needs. Therefore, you should consider the appropriateness of the advice in light of your own objectives, financial situation or needs, before acting on it. You should also obtain a Product Disclosure Statement (PDS) relating to the product and consider the PDS before making any decision about whether to acquire the product.